There has never been a better time to refinance existing debt with the SBA 504 Loan Program!

- Fixed-Interest Rates for the Life of the Loan

- Cash Out – Provide needed liquidity for eligible business expenses (W/O Expansion)

- Improve Financial Institution’s LTV

- Improve Borrower’s Cash Flow

Is Your Project Eligible?

For more information, please download our Debt Refinance Guide below.

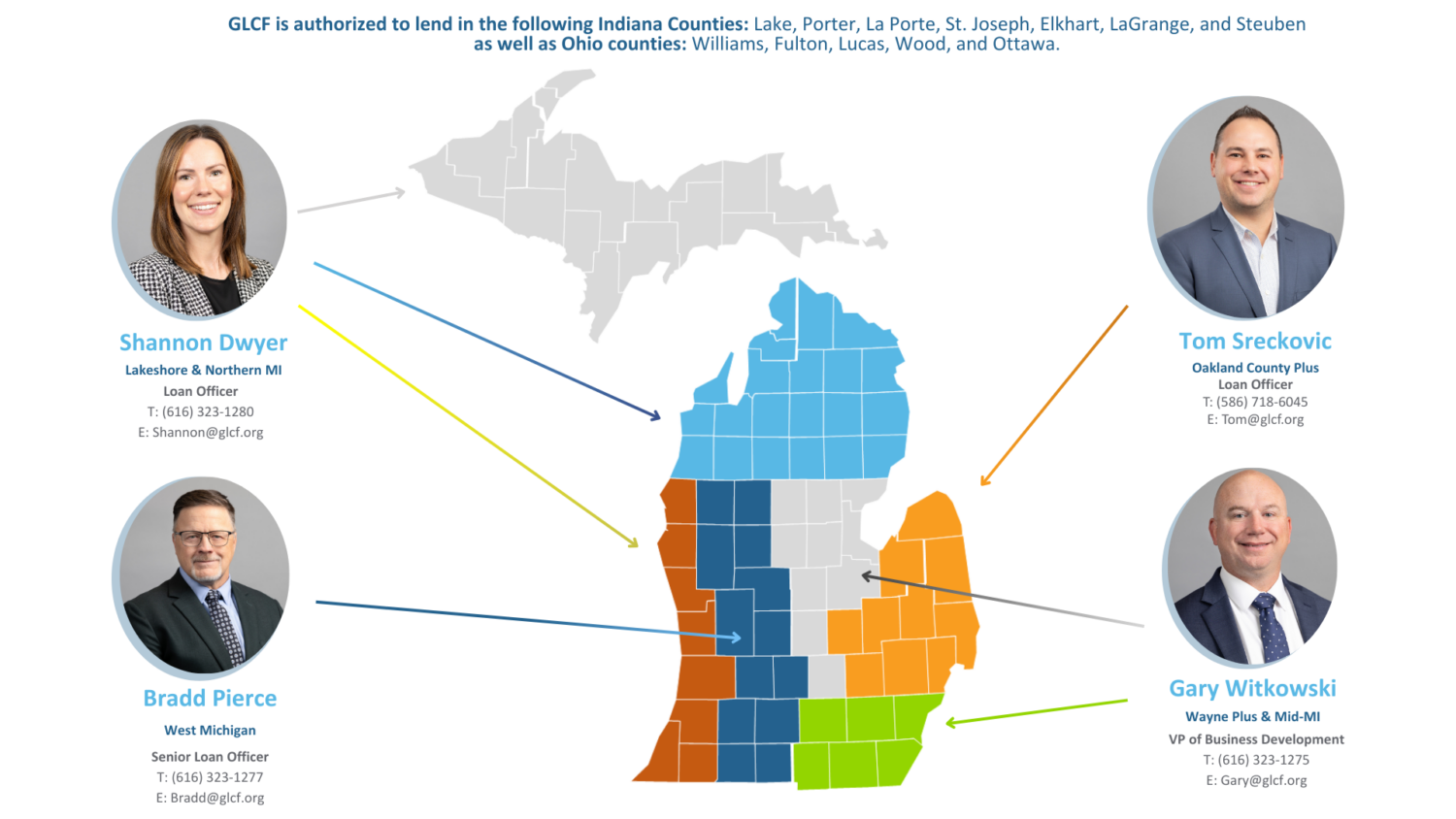

Download our 504 Debt Refinance GuideIf your project meets all the basic eligibility requirements, please contact one of our Loan Officers!

Every deal is different but the GLCF team is here to help.