1. OWN INSTEAD OF LEASE

A business owner can build equity while securing stability.

2. VALUE

With a 504 loan, a business owner can purchase real estate or machinery. They then get the tax benefits and appreciation on the real estate while locking in occupancy costs for 20 years.

3. LOW DOWN PAYMENT

A business owner knows the importance of liquidity. With financing available for up to 90% of the project cost, the 504 loan offers a 10% down payment (compared to 20-25% through a conventional loan), enabling the owner to conserve working capital.

4. GOVERNMENT-BACKED

The SBA created this program to increase the accessibility of business loans to entrepreneurs, helping to enhance the economic health of local communities.

5. LOW FEES

GLCF encourages interested small businesses to compare SBA 504 loan fees to fees of other loan options on the market, including other SBA-backed loans such as the 7(a). We feel that the 504 loan fees will compare favorably to other products, and many of the fees can be rolled into the loan.

6. LONG TERM FINANCING

Besides the low-down payment, this is probably one of the biggest advantages of the 504 program. The 504 loan means 10, 20, and even 25-year fully amortizing financing. This enables a business owner to pay for their building and/or equipment over the long term while securing them against interest rate risk in the future that happens with shorter loan terms on conventional financing options.

7. COMPETITIVE INTEREST RATES

In the last several years, 504 loan interest rates have been at historically low levels. SBA 504 loans are funded by monthly bond sales to investors on Wall Street. These bonds are backed by the guarantee of the U.S. Government which is attractive to investors and keeps rates low.

8. FIXED RATE

SBA 504 loan financing allows a business owner to fix his or her occupancy costs rather than worry about market instability that can cause a large fluctuation in floating rates.

9. FLEXIBILITY

An entrepreneur can purchase and hold title to a building personally, in the name of his business, or even set up a holding company for the real estate or equipment. This gives the small business owner the flexibility to maximize tax benefits of ownership and minimize liability in the manner best suited for them. Also, two or more businesses can receive a single 504 loan if it suits them to combine to create a real estate holding company. We have seen this option work well for professionals in the medical, veterinary, legal, and accounting fields.

10. ELIGIBILITY

Unbelievable given the advantages, a large majority of businesses and projects are eligible for the 504 program. We have worked on projects anywhere from start-up businesses to large corporations with multiple locations.

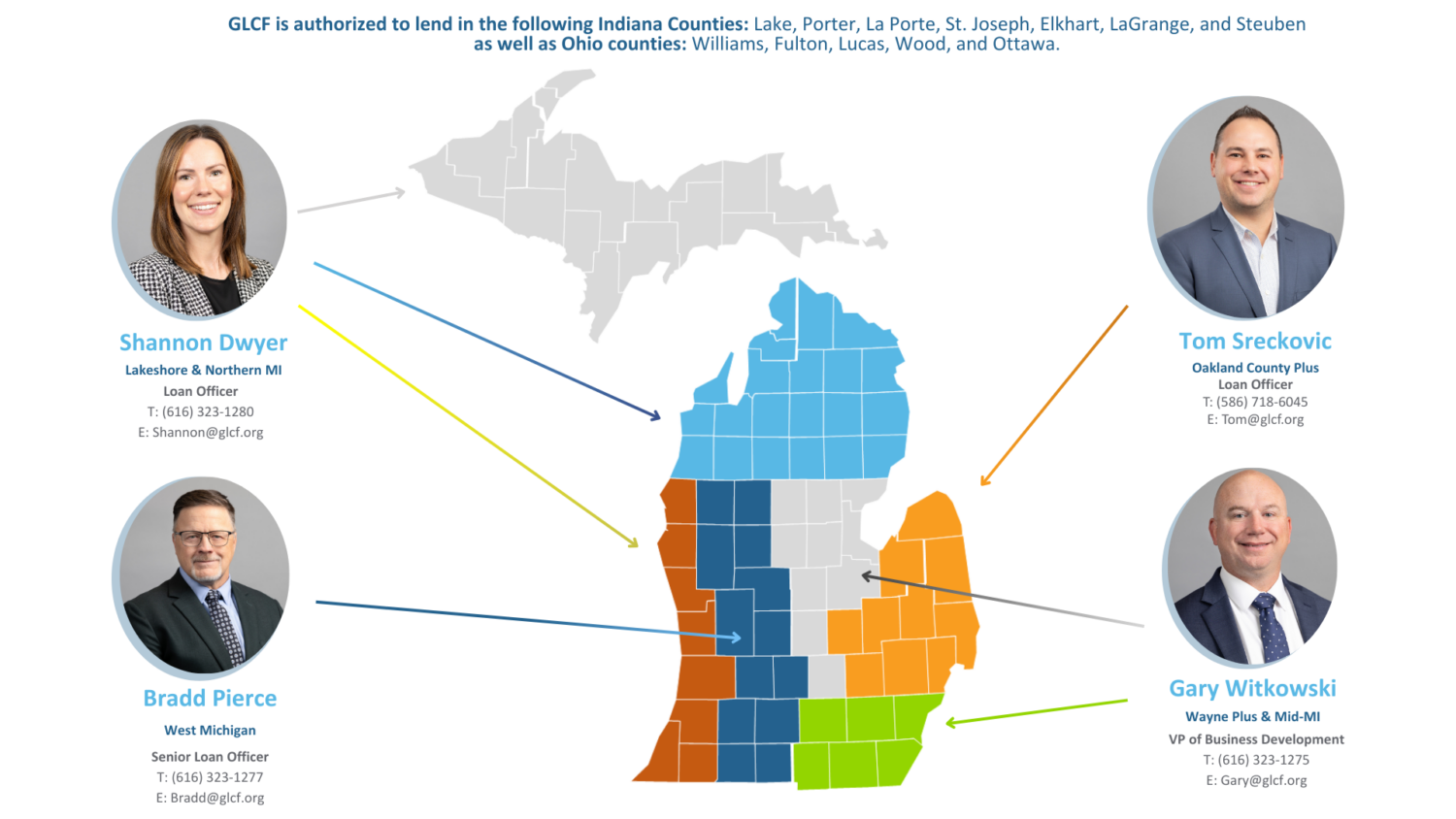

If you are interested to see if your business or customer’s business is eligible for a 504 loan, please contact one of our GLCF loan officers listed below.